Thanks for joining us!

This month’s blog is now closed. Stay up to date with the latest interest rate news on our March live blog page.

This month’s blog is now closed. Stay up to date with the latest interest rate news on our March live blog page.

Well, it was another busy news day, especially with a number of home loan rate cuts coming into effect.

Here are some of the highlights:

That’s it for today, folks! We’ll be back on Monday to update you on all things interest rates, savings, home loans and more. Have a great weekend!

Mozo has taken a close look at the number of Australians who are retiring with a home loan they still need to pay off, and the numbers are staggering.

According to data from the Australian Bureau of Statistics (ABS), 13.4% of mortgage holders in Australia are in the 65-74 age group.

This data comes from 2019-2020, and when we compared the numbers to the previous decade (2009-2010), we found that 9.3% of Aussies in the 65-74 age bracket were paying off a mortgage.

This shows a growth of 44.1% over the 10-year time period.

There are many factors that are leading to the rise of older Australians still paying off a home loan as they near or enter retirement age.

Surging house prices, delayed homeownership and life events such as divorce all play a part, but there are some moves you can make to try and help your chances.

Our personal finance expert, Rachel Wastell, says you can pay off your home loan faster by:

Think you could be getting a better rate? You can compare refinance home loans now.

Sydney’s property market is experiencing a revival in auction activity, with strong clearance rates and an uptick in scheduled auctions indicating renewed buyer and seller confidence.

More than 1,000 homes are set to go under the hammer across Sydney this weekend, according to CoreLogic’s latest Auction Market Preview . This represents a significant increase week-on-week (+9.5%) and some solid gains when compared to the same period last year (+12.5%).

Recent auction clearance rates suggest that demand remains robust. Figures for the week ending 23 February 2025 indicate Sydney recorded a clearance rate of 65.3% – the third consecutive week above 65%. Strong buyer interest has been fuelled by the February rate cut, lower-than-expected inflation and tapering borrowing charges and costs.

Key markets within Sydney are seeing heightened auction activity. Eastern suburbs and other high-demand areas like the Inner West, Northern Beaches and Blacktown are attracting strong competition, with houses and units in these areas securing solid results. Reports indicate that some properties are selling well above reserve prices, a trend that suggests buyers are willing to act quickly amid limited stock.

A number of factors are contributing to the resurgence in auction sales:

While auction volumes are expected to fluctuate in coming weeks, the latest data suggests Sydney’s property market is set for a busy autumn selling season. Buyers appear motivated to secure properties following the latest rate cut, and sellers are capitalising on strong demand.

However, prospective buyers should remain vigilant, as market conditions can change quickly depending on economic and policy developments. Check out Mozo’s Experts Choice Award Winners and evaluate rates, fees and other features using our comparison tables.

A number of banks have reduced standard variable savings rates (base rates) in response to the RBA’s first cut to the cash rate in four years.

If you rely on bonus interest to maximise savings, this concerns you.

ING’s popular Savings Maximiser account has undergone a major shake-up. While its highest variable rate will drop to 5.40% p.a. (down from 5.50% p.a.), the bank shifted the weight of its offer to the bonus rate.

For those who meet the monthly deposit and transaction conditions, ING’s account remains competitive. However, anyone who misses out will see earnings plummet, as the new base rate is barely above zero.

These changes reinforce findings from the Australian Competition and Consumer Commission (ACCC). In the first six months of 2023, 71% of bonus accounts didn’t receive any bonus interest in a given month.

The ACCC illustrated how costly this can be. For example, a saver with $5,000, depositing $200 per month could earn $328 in interest over a year at 5.25% p.a., provided they meet all the bonus conditions. These earnings sink to just $18 over the same period on a base rate of 0.30%.

For those who consistently meet bonus conditions, these accounts still offer some of the best returns on the market. However, if you struggle to hit required targets, you could wind up with next to nothing in interest.

By cutting the base rate but keeping the headline rate high, banks are maintaining the appearance of a competitive offer, but savers may find it harder to meet bonus conditions and earn the full rate.

Even if the headline rate is over 5 percent, getting stuck with a very low base rate could leave savers feeling the sting. Bonus rates can be attractive if you meet the conditions, but if you don’t – you’re missing out on most of the interest you think you’re getting.

– Mozo finance expert Rachel Wastell

If you’re using a bonus saver account, now might be a sensible time to check whether you can realistically meet the monthly conditions. If not, you may be better off shopping around for an account with a higher standard variable rate – before more banks follow suit with cuts.

Today’s newly revised Banking Code of Practice provides important protections for banking customers and small businesses.

The updated Code, approved by the Australian Securities and Investments Commission (ASIC) in June 2024, strengthens protections for customers in certain areas, particularly for people experiencing vulnerability.

It also reinforces the commitment of banks to responsible and fair conduct.

Briefly, the changes include:

Importantly, the Code retains key protections such as the diligent and prudent banker obligation, ensuring an ongoing focus on appropriate lending.

Of the changes, Australian Banking Association chief, Anna Bligh says this was a Code "with teeth" and raises the bar even higher.

"This new rule book is about ensuring that when customers interact with their bank, they are getting the highest level of service and care," Bligh said.

"It sets new standards and clearer expectations for service, integrity and accountability across the entire banking industry.

"There is now greater clarity on how banks will support customers facing financial difficulty, including arrangements that can be put in place to help them get back on their feet."

Stay up to date on all the latest banking and rate news right here on the Mozo live blog. You can also check the latest rate movements on our live rate change tracker!

Bankwest has cut rates by up to 0.25% across its savings products, joining other banks following the recent interest rate changes.

Bankwest's Hero Saver account has reduced the standard rate by 0.05%, and the ongoing rate has been cut by 0.20% for balances up to $250,000, and by 0.05% for balances up to $5 million.

The Easy Saver account has had the standard variable rate cut by 0.15% and the introductory rate reduced by 0.20%.

For Retirement Advantage account holders, rates have been lowered by 0.15% for balances up to $49,999.99 and by 0.25% for balances of $250,000 or more.

Check Mozo’s rate change tracker for more interest updates.

With variable home loan rate changes hitting today for three of the big four banks, we thought it time to consider how choosing a better-than-average rate can save you money.

We know from our Mozo Experts Choice Awards (MECA) analysis done in early February that the average variable rate (owner-occupier, P&I, 80% LVR, $500k) is 6.71% p.a. for a monthly repayment of $3,441.

Meanwhile, the average variable rate for a big four home loan (owner-occupier, P&I, 80% LVR, $500k) is notably higher at 7.15% p.a. for a monthly repayment of $3,582.

Now here's the good bit: the average variable rate of MECA winning products (owner-occupier, P&I, 80% LVR, $500k) is 6.01% p.a. for $3,224 per month - significantly lower.

All up, the big four rates are 19% (or 1.19%) higher than average, while our MECA winners are 16% (or 0.84%) lower.

This difference should be top of mind as you compare home loans. Even if your big four home loan rate drops by 0.25% p.a. with the recent RBA rate cut, be sure to check how the new rate compares to the market.

Check Mozo’s rate change tracker for more interest updates.

One of the big four banks, CommBank, has cut rates for its Business Online Saver, ranging from 0.05% to 0.10%, depending on the account balance:

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

CommBank, Australia's largest bank, has cut rates by up to 0.25% across its savings products, following the recent Reserve Bank of Australia (RBA) rate decision.

CommBank's Youthsaver account has received a headline cut of 0.25%, bringing the total interest rate to 4.75%. This change includes a 0.20% reduction to the base rate (now 2.40%) and a 0.05% cut to the bonus rate (now 2.35%).

The GoalSaver account has also been reduced with a 0.25% headline cut, resulting in an ongoing bonus rate of 4.65%. This includes a 0.05% reduction to the base rate (now 0.35%) and a 0.20% cut to the bonus rate (now 4.30%).

For NetBank Saver customers, the introductory rate has been lowered by 0.20%, now offering 4.90% for the first 5 months, before reverting to 2.15%. The base rate has been cut by 0.20%.

Check Mozo’s rate change tracker for more interest updates.

Heads up - Macquarie Bank cut its Savings Account rates by 25 basis points today, the bank has announced.

Here are the details in brief:

See our full coverage and check Mozo’s rate change tracker for updates.

Good morning and welcome back to our live coverage of interest rate and banking news!

Hot off the press today, three of the Big 4 banks have new home loan rates that come into effect today.

CommBank, NAB and ANZ have all adjusted their variable home loan interest rates by 0.25% p.a. and these cuts are effective now, 28 February, 2025.

Also going live today, ANZ Plus, Macquarie, Bankwest, Ubank and Suncorp, are all dropping variable home loan rates by 0.25%.

Finally, Auswide Bank, Firefighters Mutual Bank, Health Professionals Bank, Homestar, Police Bank, Resi, Sucasa, Teachers Mutual Bank and UniBank are also cutting rates by 0.25% as of this morning.

You can find some of the leading home loan rates in the Mozo database on our home loans hub page.

That’s a wrap on today’s live blog – here’s a recap in case you missed it:

Join us again tomorrow for more interest rate and banking news as it happens. You can also check Mozo’s interest rate tracker to see which lenders have so far passed on the interest rate cut to borrowers.

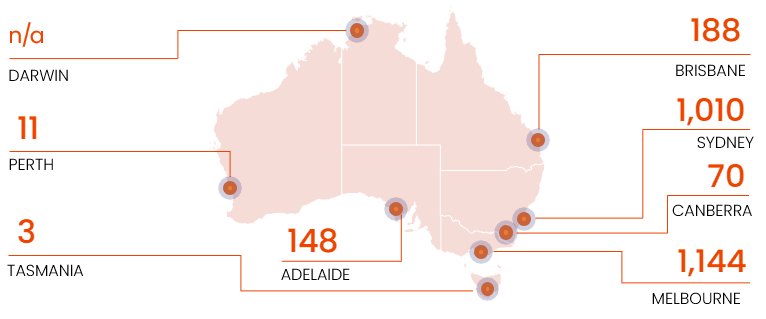

There are now more cities under mortgage stress than there were five years ago, according to a new report released by Domain .

Mortgage stress is typically defined as when a person is paying more than 30% of their pre-tax income on home loan repayments.

Domain’s report found that when it came to entry-priced houses, all of Australia’s capitals are now causing mortgage stress for first home buyers, with the exception of Darwin.

For units, there were no cities experiencing mortgage stress five years ago. Now, Sydney, Brisbane and Adelaide have crossed the threshold, and first home buyers are seeing more than 30% of their income going towards repayments.

The difference between saving for an entry-priced house and an entry-priced unit is also quite stark.

Across all of the capitals, Domain found that borrowers can save a 20% deposit almost two years quicker (20 months) than it could take them to save for a deposit on an entry-priced house.

In Sydney, you can potentially get into the market 2 years and 5 months faster if you want to buy an entry-priced unit compared to an entry-priced house, while in Canberra the time difference is 2 years and 4 months faster for a unit.

This is why with recent changes, it’s more important than ever to compare home loans and search for a better deal – potentially one with a lower rate of interest and lower fees.

Back-to-back rate cuts are likely off the table says NAB’s chief economist, Alan Oster. On this week’s NAB Broker podcast , he forecasts the Reserve Bank of Australia (RBA) will trim the cash rate again in May, followed by more cuts in August and November – taking it to 3.10% by early 2026.

We expect another one early next year as well because we think you should have a cash rate back towards neutral, somewhere around 3%.

– NAB chief economist Alan Oster

This comes after the RBA’s 25 basis point cut earlier this month, which Oster labelled a “hawkish cut” – essentially, a rate drop with a warning that the central bank isn’t rushing into more unless the data stacks up.

The latest monthly inflation figures show annual CPI growth at 2.5% in January. This suggests the economy is cooling, however, core or “trimmed” inflation ticked up slightly (+0.1%) to 2.8% in January.

While markets are betting on more cuts, RBA Governor Michele Bullock has made it clear they’ll take things one step at a time. So while lower rates might be on the way, don’t expect things to change in a hurry.

For mortgage holders, that means some potential relief ahead – but for savers, it could signal the end of high deposit rates. Either way, all eyes are on the RBA as we move into the next phase of the rate cut cycle.

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

As we’ve reported on this week, many cuts to savings account interest rates have already come into effect, whereas cuts to home loans are coming a bit later.

We’ll start to see some of the big names reducing their home loan interest rates from Friday, 28th of February (that’s tomorrow).

So, why has there been a delay between savings account interest rates dropping, and mortgage holders finally getting some relief?

Mozo’s finance expert, Peter Marshall, says this is fairly standard practice for the banks.

“Following a cut to the cash rate, banks will usually change savings rates a little faster than they do for their home loan rates,” he says.

“This means that they reduce the amount of interest they are paying to savers before people with a mortgage get to reduce their interest payments, helping the banks to make some extra profit on their interest margins.

“As home loan rates are being cut quite quickly this time around the delay is not large, but most banks are still cutting rates for savers a little faster than for their home loan customers.”

Below, we have some tables that indicate the potential savings lost due to the cuts to savings accounts, and the savings that could be earned thanks to home loan interest rates being reduced.

| Average rate (p.a.) | Total interest after one year | Average rate after cut (p.a.) | Total interest after one year | Savings loss | |

|---|---|---|---|---|---|

| Ongoing @ 10k | 3.53% | $10,359.00 | 3.28% | $10,333.00 | $26.00 |

| Ongoing @ 25k | 3.53% | $25,897.00 | 3.28% | $25,832.00 | $65.00 |

| Ongoing @ 50k | 3.53% | $51,794.00 | 3.28% | $51,665.00 | $129.00 |

| Bonus @ 10k | 4.58% | $10,468.00 | 4.33% | $10,442.00 | $26.00 |

| Bonus @ 25k | 4.58% | $26,169.00 | 4.33% | $26,104.00 | $65.00 |

| Bonus @ 50k | 4.58% | $52,339.00 | 4.33% | $52,208.00 | $131.00 |

| Source: Mozo database as at 27 February 2025, average saving rates vs average saving rates after RBA cut at $10,000, $25,000 and $50,000 balances. | |||||

| Average rate (p.a.) | Monthly repayment total | Average rate after cut (p.a.) | Monthly repayment total | Savings earned | |

|---|---|---|---|---|---|

| Variable @ $400,000 and 80% | 6.72% | $3,445.00 | 6.47% | $3,367.00 | $78.00 |

| Variable @ $500,000 and 80% | 6.71% | $3,442.00 | 6.46% | $3,364.00 | $78.00 |

| Source: Mozo database as at 27 February 2025, average variable home loan vs average variable rate after RBA cut for owner occupier, principal & interest home loans at $400,000 and $500,000, at 80% LVR. | |||||

With the RBA recently reducing the cash rate to 4.10%, some savings accounts and term deposit rates have seen adjustments downward.

Term deposits at least offer a financial fortress for locking in rates.

For example, NAB and ANZ currently lead the Big Four with 4.20% p.a. on 1-year term deposits, while CommBank offers 4.15% p.a. and Westpac offers 4.00% p.a. for the same term.

Looking beyond the Big Four could yield bigger rates though. For example, smaller providers like Heartland Bank's 1-year term deposit sits at a much higher 4.90% p.a. and is 70 basis points higher than NAB's equivalent account. For longer terms, Judo Bank's 4.50% p.a. 5-year term deposit is 110 basis points higher than Westpac's 3.40% p.a. 5-year term.

These could be worth exploring to at least lock in some of your savings.

Want to explore all your options? Check out our comparison of Big Four term deposits here.

Yet another bank has cut savings rates in light of the cash rate cut, with ING making cuts across its savings product range effective tomorrow.

ING's Savings Maximiser will see its conditional headline bonus rate drop by 0.10% to 5.40% p.a. for customers who meet the monthly eligibility criteria. The base rate will also decrease by 0.05% to 0.55% p.a. for new and existing customers.

ING's Savings Accelerator will see rate reductions, with standard variable rates dropping by 0.25% across all balance tiers:

The Savings Accelerator Kick Starter offer for eligible savers will see similar reductions:

ING's Business Optimiser hasn't escaped the cuts either, with the 6-month variable welcome rate for new and existing eligible customers decreasing to 0.75% p.a., while the standard variable rate will drop to 0.35% p.a.

Despite these reductions, ING's top conditional rate of 5.40% p.a. on the Savings Maximiser sits well above the database average. However, savers should note that this rate requires meeting monthly eligibility criteria, unlike some institutions offering condition-free rates.

Be sure to check out Mozo’s live tracker to see which lenders passed on rate cuts.

Good morning and welcome back to the Mozo live blog, where we unpack how the recent rate cut could impact your finances.

With the RBA lowering the cash rate to 4.1%, borrowers will see some relief, but CoreLogic’s Tim Lawless says the broader impact on housing is more complex. While sentiment is improving, affordability remains stretched, and further rate cuts aren’t guaranteed.

Here’s how he sees it playing out:

In other words, the housing market is adjusting, but with affordability still tight and economic uncertainty ahead, Lawless expects a gradual recovery.

Stay on track with the live tracker.

As we wrap up today's live blog coverage, here are the key highlights:

Join us tomorrow for more live finance news and check Mozo’s live tracker to see which lenders have passed on the rate cut to borrowers.

With the Reserve Bank of Australia (RBA) lowering interest rates, property markets across the country are poised for change. Three cities are set to benefit most from the RBA’s shift in monetary policy, according to a unique, in-depth analysis by Australian buyer’s agency InvestorKit.

Sydney’s property market has historically been highly sensitive to interest rate movements. InvestorKit notes that housing inventory levels remain low, at around three months, meaning demand is likely to rise as borrowing conditions improve. The rate cut could also restore buyer confidence, increasing competition and potentially driving price growth.

The city has maintained a consistently low housing inventory of around two months for the past two years. Rental vacancy rates sit at around 1%, indicating strong demand. Research suggests that while Newcastle's property prices haven’t always been responsive to interest rate changes, the combination of low supply and easing affordability may spur growth.

The housing market has been bolstered by affordability and lifestyle appeal, making it attractive for buyers priced out of Melbourne. The research highlights that property prices have remained resilient despite high interest rates. With borrowing costs softening, demand is expected to rise, sustaining price growth and making it a market to watch.

Key takeaways:

If you're looking to purchase in these or other markets across Australia, securing a competitive home loan is key to maximising your buying power. Mozo’s home loan comparison tables make it easy to compare rates, fees, and features across a range of fixed and variable mortgages.

Following the RBA’s cash rate cut, a number of lenders announced that they would be reducing rates on eligible business loans, including Commonwealth Bank of Australia, The Mutual Bank and IMB Bank.

For small and medium enterprises (SMEs) with existing loans or those looking to borrow, reduced interest can offer more affordability, easing cash flow pressures and creating avenues for investment and expansion. However, rate cut impacts may be gradual rather than immediate, as inflation and operational expenses are still tough, ongoing challenges.

A recent national survey by specialist small business lender OnDeck highlights strong optimism among small business owners.

The survey was conducted prior to the RBA's rate cut. SME confidence is expected to rise even higher following the shift in monetary policy.

The federal Opposition recently proposed significant changes to APRA’s lending criteria to make business finance more accessible. One of the key measures includes removing the requirement for homeownership as collateral for business loans. This aims to eliminate a major barrier for entrepreneurs who do not own property but have viable business plans.

There's also plans to adjust APRA’s serviceability requirements to make it easier for SMEs to access funding. Easing these restrictions may encourage greater investment, spur economic growth, and create more opportunities for businesses to access credit and get off the ground.

Reduced loan interest charges and potential regulatory changes may help if you're starting or growing your own SME. Doing some research and comparing business loans can help you to find the best deal.

Hot off the press, the monthly consumer price indicator rose 2.5% in the 12 months to January, the Australian Bureau of Statistics reports today.

In economics 101 classes everywhere, this will be called a ‘steady’ result.

The top contributors to price movement were food and non-alcoholic beverages (+3.3%), housing (+2.1%), and alcohol and tobacco (+6.4%).

Partly offsetting the annual rise was a fall for electricity (-11.5%).

While the headline number was steady, core or “trimmed” inflation moved up 2.8% in January following a 2.7% rise in December.

By this measure, this is a slight move in the wrong direction given recent hopes that inflation has come under control.

However, most of the analysis this morning suggests that the RBA will be comfortable with this result and will feel vindicated in cutting interest rates by 0.25% p.a. at its recent policy meeting.

It’s also worth noting that the RBA tends to focus on quarterly inflation results rather than monthly.

The target range for inflation is 2-3%, as set by the RBA. With these latest numbers, which report the year to January it should be again noted, it seems there's a lid on most costs.

Of course, we should also note that the “trimmed inflation” figure (up 2.8%) is an alternative measure of underlying inflation that reduces the impact of irregular or temporary price changes at the top end and low end of costs.

"Should Q1 data bring further disinflation, we can look to May as the next time Michele Bullock and her team may cut rates." - Josh Gilbert, eToro

Some of these numbers start to run together, so let’s turn to an expert for a bit of perspective.

Market analyst at eToro, Josh Gilbert says this outcome doesn’t necessarily provide a smoking gun for the RBA to continue cutting rates, but it does offer reassurance that inflation is moving in the right direction and supports the [rate] cut we saw earlier this month.

"The biggest concern for policymakers and investors alike remains the view that disinflation may stall, hence the RBA’s hawkish stance despite cutting rates," Gilbert says. "We’ve seen this happen across the pond, where price pressures have persisted in the US and the Fed is easing off when it comes to cutting rates.

"For now, another cut isn’t likely in April, particularly with the ongoing strength in the labour market. The board will be laser-focused on Q1 data released after its decision in April. Should that bring further disinflation, we can look to May as the next time Michele Bullock and her team may cut rates."

Be sure to check out Mozo’s live tracker to see which lenders passed on rate cuts.

Just in, Abal Banking is cutting its variable rate home loans by 0.25% as of 4 March, following the RBA’s rate cut decision.

Abal is a wholly owned subsidiary of Arab Bank, the first private sector financial institution in the Arab world, with over 80 years in the business. Arab Bank says it has the largest Arab banking branch network in the world with more than 600 branches spanning five continents.

You can find some of the leading home loan rates in the Mozo database on our home loans hub page.

Credit Union SA has announced it will pass on the full 0.25% RBA rate cut to reduce all existing member variable home loans and line of credits from 5 March, 2025.

Credit Union SA offers a number of variable rate home loans, some of which are Mozo’s Experts Choice Award winners in 2025.

Credit Union SA is the merger of two South Australian credit unions in 2009 and has more than 50,000 members, according to its website.

Stay on track! Check Mozo’s rate change tracker for updates.

Good morning and welcome back to our ongoing coverage of Aussie interest rates and how the recent rate cut by the RBA will impact your finances.

With the RBA’s decision having sunk in, many customers will now be considering a banking switch.

Roy Morgan has done some research on this and notes that in the past 12 months (to February), Aussies are primarily switching due to poor interest rates, poor service and high fees.

The data shows that Macquarie and the newer digital banks such as ANZ Plus, ME Bank, Ubank and Up have been the main beneficiaries of this ‘switching’ in the last 12 months.

About 667,000 Australians (3%) have switched their main financial institution in the last year, Roy Morgan reports.

These customers may not have cancelled accounts or opened new accounts – but they have changed the bank they consider to be their main one.

Specifically, Macquarie gained 48,000 customers and lost only 5,000 for a net gain of 43,000, while the newer digital banks (ANZ Plus, ME Bank, Ubank and Up) gained 60,000 and lost 29,000 for a net gain of 31,000.

The big four banks and ING saw little change, with gains and losses about equal. Regional banks lost an estimated 21,000 customers through switching (gaining 79,000, while losing 100,000).

Roy Morgan general manager of financial services, Suela Qemal says that among those switching from a big four bank to a digital bank, 40% cite poor interest rates as the main reason, followed by 35% who point to poor service, and 22% who mention high fees.

“Digital banks are benefiting from offering better interest rates, which is particularly appealing during the ongoing cost-of-living crisis,” Qemal said.

“In 2024, digital banks gained ground by attracting customers with their deposit products but are now shifting focus to mortgages. This trend is expected to grow in 2025, especially with younger customers seeking better financial solutions.”

Be sure to check out Mozo’s live tracker to see which lenders passed on rate cuts.

Never a dull moment over here at the Mozo's live blog! Here’s what we covered today:

And that does it for today! Meet us here tomorrow: same time, same place, where we update you on all things interest rates, savings, home loans and more - all as it happens!

The RBA’s latest rate cut offers clear benefits for borrowers, with lower home loan rates directly reducing mortgage repayments. But while savers might expect to lose out as banks cut savings rates, those who act quickly can still get ahead.

While borrowers get the immediate win, savers still have options if they’re proactive.

Gateway Bank is cutting its variable home loan and reverse mortgage rates by 0.25% p.a. following the RBA’s recent rate decision, with the new rates taking effect from Tuesday, 25 February 2025. The change applies to both new and existing borrowers.

Here’s what’s happening:

How will this impact your repayments?

For any questions or help reviewing your loan, log into online banking or get in touch with Gateway Bank.

Here at Mozo, we’re tracking all these changes live, so to see which lenders passed on rate cuts, head on over to Mozo’s live tracker!

Interest rates on savings accounts are continuing to drop, with Rabobank decreasing its rates by 0.25%.

Rabobank’s High Interest Savings Account now comes with a base rate 4.10% p.a., which is still above the average when it comes to the base rates tracked in our database.

For example, the average ongoing savings rate across our database – bonus rates included – is 3.53% p.a. (as at 25 February, 2025).

So while Rabobank has dropped its savings rate, it’s still higher than average and comes with no conditions attached, such as a minimum deposit amount or spending requirements.

Rabobank’s 4-month introductory bonus rate is now 5.45%, though this has only dropped by 0.15% p.a. for new customers – effective today.

One of Australia’s largest customer-owned banks, Great Southern Bank has reduced savings rates by 25 basis points on a number of its products, effective as of today.

Some of the accounts that will be affected are the Everyday 50+, Home Saver, Goal Saver, eSaver Flexi, Advantage Saver, Youth Saver, and Future Saver, according to the bank’s website.

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

Queensland Country Bank has announced a reduction in its variable home loan interest rates by 0.25% p.a. with this adjustment taking effect on Tuesday, March 11, 2025.

Lenders have adopted different timelines for when their anticipated rate cuts will become effective, with some institutions implementing changes in the coming days, while others plan to roll out adjustments into next month.

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

Welcome to Mozo's ongoing coverage of interest rates and how the RBA's latest monetary policy decision affects your money moves.

In an environment where inflation currently sits at 2.4% , many savers may find that their bank accounts aren’t keeping pace with the rising cost of living. While it’s easy to assume that a high interest rate on your savings will yield solid returns, the reality is that it’s crucial to regularly review the interest rates offered on savings accounts. Here’s why:

Using Mozo’s data to break down savings account rates offered across various categories, we can see how they compare to the inflation rate:

Now, these rates might seem reasonable, however, they don’t factor in the annual rate of inflation – 2.4% in December 2024. When adjusted for inflation, the real return (i.e., the actual purchasing power) can be significantly lower than you might realise.

For instance, if you have $10,000 in a savings account offering an ongoing rate of 3.53% p.a., you're earning $359 annually. But once inflation is accounted for, your money’s purchasing power is eroded by the inflation rate. In practical terms, you’re only seeing a real return of around 1.13% p.a. or about $114 per year. So, while your balance grows, it may not be keeping up with the increasing costs of goods and services.

For savers earning the lowest average unconditional rates (1.43% p.a.) or Big Four base rates (1.15%), real rates of return are in negative territory.

While introductory and bonus rates may appear to offer a better deal upfront, they often have short-term benefits. It’s important to factor in the length of time these offers are available and whether you meet the conditions to earn those higher rates. Over time, you may find yourself locked into lower returns once the intro or bonus period ends.

By shopping around and comparing savings account interest rates, you may discover better returns. You may also want to consider alternative savings options. Laddering term deposits could allow you to lock in higher rates over different timeframes, diversifying your investment and reducing the impact of rate changes. You may also want to explore other investment products that could yield you higher returns over time.

Learn about the cash rate decision and check out Mozo’s live tracker to see which lenders passed on a cut to borrowers – and which haven’t.

| Savings Accounts | Average | Median | Best |

| All Personal Accounts – $10,000 balance | |||

| All Ongoing | 3.53% | 4.18% | 5.50% |

| Only Bonus | 4.59% | 4.70% | 5.50% |

| Only Introductory Rates | 4.95% | 5.05% | 5.45% |

| Only Unconditional Rates | 1.43% | 0.83% | 5.10% |

| Big Four – $10,000 balance | |||

| Ongoing Bonus | 3.24% | 3.23% | 5.20% |

| Only Bonus | 4.75% | 4.90% | 5.20% |

| Only Introductory Rates | 4.63% | 4.88% | 5.10% |

| Only Base Rates | 1.15% | 1.25% | 2.35% |

Source: Mozo database as at 25 February, 2025.

Property expert and managing director of SQM Research, Louis Christopher says he now expects a turn around in the fortunes of the Sydney and Melbourne housing markets, following the RBA’s recent 0.25% rate cut.

"If I’m right, we should see a lift over the next four weeks in auction clearance rates for these two cities," Christopher said. "On our measure of clearance rates, we could see a rise in both cities to the 50% to 60% range.

"After the initial falls recorded so far this year, I expect Sydney housing prices to finish the year up by between 3 to 7% and Melbourne up modestly by 2 to 6%."

Christopher adds that with rental markets remaining tight in most capital cities, he also expects to see a lift in first-home buyer activity.

"The rate cut, with a high probability of another to occur at the beginning of April, not only provides some relief to existing borrowers but also will provide some confidence to home buyers that interest rates are finally heading down - and certainly not going up.

"It immediately lifts their borrowing power with the banks given better servicing on a lower interest rate."

Christopher says Perth and Brisbane are still tipped to be the top performing markets, followed closely by Adelaide.

That's a wrap for today! Join us again tomorrow for more interest rate and banking news - live as it happens! You can also check Mozo’s live tracker to see which lenders have so far passed on the interest rate cut to borrowers.

The recent cut to the cash rate provides some relief for mortgage holders, but for renters, the situation remains tough. With lease costs high and rising, many are struggling to keep up.

At a parliamentary inquiry on Friday, RBA Governor Michele Bullock pointed out that renters, particularly those with lower incomes, were among the hardest hit by the cost-of-living crisis.

“That would be, I think, the group that is often forgotten. I just want to make sure that people understand they are people that have really been hurt very hard by this.”

“They’ve seen a massive increase in rents and they’ve also experienced massive inflation. So they’re not going to necessarily benefit from the decrease in rates. They are going to benefit as inflation starts to come down, and it is coming down, so that’s beneficial for them.”

– RBA Governor Michele Bullock

While the rate cut helps homeowners with mortgage repayments, it does little for renters facing skyrocketing housing costs. Australian Bureau of Statistics (ABS) stats revealed rents increased 6.4% over the 12 months to December 2024, making it increasingly difficult for low-income renters to save for a future home or even afford current living arrangements.

Here’s what renters can do in light of the RBA’s decision:

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

The Reserve Bank’s latest rate cut won’t see most mortgage holders reducing repayments. Instead, ING research shows more than two thirds (68%) of borrowers plan to keep making the same repayments, using the opportunity to get ahead on their home loans.

Of these, over half (56%) will be directing extra funds towards paying down their principal, helping them build equity faster, while two fifths (43%) said they’ll put any extra savings into an offset account to reduce interest costs over time.

This proactive approach suggests that many Australians are prioritising long-term financial stability over short-term relief, but it also raises questions about whether lenders will introduce more attractive deals to encourage refinancing or rate negotiations.

ING’s findings also revealed other notable financial moves:

Interested in paying off your home loan faster and cutting interest costs? Use our extra repayments calculator to see how much you can save.

If you’re seeking a more competitive home loan or are interested in refinancing your current mortgage, it can pay to compare your options to ensure you find the best deal that suits you.

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

Just in, Aussie will decrease its variable home loan interest rates by 0.25% p.a for new and existing customers, the mortgage provider says.

The details for each home loan product are as follows:

Aussie Elevate home loan customers

Aussie Select home loan customers

For Aussie Activate home loan customers

See Mozo’s live tracker to see which other lenders are passing on rate cuts.

NAB has today announced that homeowners can offset their mortgage by using up to 10 separate accounts with a new feature in the bank’s app, potentially saving them a lot on interest.

The reason for this move is simple: demand for offsets by NAB customers has increased since the pandemic, with around 70% of new homeowners now choosing to offset their loan, NAB says.

In fact, offset balances have grown by 65% to $48 billion, the bank reports.

NAB executive Andy Kerr says the home loan feature is suitable for Aussies who split their funds across several accounts.

"Many Australians bucket their money into different categories to manage their budgets,” said Kerr. "With multiple offset accounts, they can continue doing this while also saving even more on their home loan interest. They no longer have to sacrifice one for the other."

Keep in mind that NAB isn’t the only bank providing multiple offset accounts - three of the big four banks do so.

Last week, Westpac introduced the option for 10 accounts for its home loan customers.

Westpac managing director of mortgages, Damien MacRae said the bank has also seen a steady increase in customers building up their offset balances.

"Multiple offset accounts give you the flexibility to bucket finances for different purposes,” he said. “An example of this could be setting aside money in separate offset accounts for everyday living expenses, a holiday or emergency funds.”

CommBank similarly offers multiple offset accounts, however ANZ does not.

Other well known banks to offer multiple offsets include Macquarie, Suncorp, Ubank and Up.

Mozo finance expert, Rachel Wastell says the feature is very useful because even your regular income or everyday spending money can sit in an offset account to help reduce your home loan costs.

"With multiple offsets, homeowners have the benefit of bucketing savings accounts to easily track different goals or allocate expenses - all the while reducing the interest charged on their home loan," Wastell says.

"The reality is, even your paycheck, emergency fund, or everyday spending money can be put to work in an offset account. A dollar in an offset can be as powerful as it reduces the interest you pay, with the added bonus of flexibility. And you can still access your money when you need it."

Learn more about the recent RBA decision and check Mozo’s live tracker to see which lenders passed on the interest rate cut to borrowers.

Regional Australia Bank is also passing on the full 0.25% cash rate decrease to existing members on variable rate home loans, the lender says.

This change will be effective from 4 March, 2025.

Regional Australia Bank advises customers with a variable rate principal & interest home loan to find new minimum repayment details on their next statement or via the Your Banking app from 4 March.

Regional Australia Bank (previously known as Community Mutual Group) is a member owned lender that has been providing Aussies with finance solutions for over 45 years.

Just in, QBANK's variable rate home loans will decrease by 0.25% p.a., effective 11 March 2025, the lender says.

QBANK (formerly QPCU) provides specialised products for the Queensland police force, fire and rescue service personnel, ambulance officers, SES personnel, public sector employees and their families.

It offers home loans for owner-occupiers, first homebuyers and investors.

QBANK was also awarded as Australia's Best Specialist Customer Owned Bank for the 2023 Mozo Experts Choice Awards.

See Mozo’s live tracker to learn which lenders are passing on rate cuts.

Good morning and welcome back to our ongoing coverage of Aussie interest rates and how the recent rate cut by the RBA will impact your finances.

To start with, Commonwealth Bank will cut interest rates by 0.25% p.a. on eligible business lending products, following the RBA's decision last week to drop the official cash rate by 0.25% p.a.

CBA's Business Bank will be reducing interest rates across its variable base rate, residential equity rate, and overdraft reference rate by 25 basis points, the bank reports.

This reduction will apply to business lending products including Better Business Loans and Business Overdrafts. All business loan variable rate changes announced will be effective 28 February, 2025.

CBA group executive business banking, Mike Vacy-Lyle says businesses are the lifeblood of Australia’s economy, and they’ve shown remarkable resilience in what has been a challenging environment.

"While these rate reductions may provide some relief, we recognise some of our business customers are facing challenging times and we have a range of measures available for businesses facing difficulty, such as waiving merchant terminal rental fees and deferring repayments on business loans," Vacy-Lyle said.

"We also recognise the importance of balancing the needs of business borrowers and business depositors, and we will continue to review our pricing and make further adjustments as required."

Learn more about the recent RBA decision and check Mozo’s live tracker to see which lenders passed on the interest rate cut to borrowers.

It was another busy day of rate change news today, here’s what we covered:

Okay, that’s a wrap for today! Thanks for joining us this week and we look forward to bringing you more interest rate news next week. Have a good weekend!

Dozens of lenders are set to cut their home loan interest rates by 0.25% in the coming weeks, but some providers have been quick to reduce the interest earned on their savings accounts with immediate effect.

As a quick refresher, when the Reserve Bank lowers the cash rate, lenders can pass on the cut to its home loan customers – but the banks can also reduce the interest rate earned on its savings accounts.

In fact, Mozo’s database shows that some banks are cutting their deposit rates by up to 0.35% – that’s more than the RBA’s official rate cut of 0.25%.

NAB, AMP, Bank of Queensland and ME Bank have each introduced cuts to their savings rates effective from today (21 February). See our table below for a breakdown.

| Bank | Savings rate cut (% p.a.) effective today | Home loan rate cut effective date | Days between savings and home loan rate cuts |

|---|---|---|---|

| NAB | Reward Saver + iSaver: -0.25% | 28 February 2025 | 7 days |

| AMP | All at-call deposits: -0.25% 31-day Notice Saver: -0.35% 6-month Notice Saver: -0.25% | 3 March 2025 | 10 days |

| BOQ | Future Saver, Smart Saver: -0.25% Kids Savings Account: -0.25% Simple Saver: -0.30% | 7 March 2025 | 14 days |

| ME Bank | SaveME: -0.25% | 8 March 2025 | 15 days |

For the remaining three major banks, ANZ has yet to announce any cuts to its savings rates, but it will be cutting home loan interest rates on 28 February.

CommBank and Westpac have both announced cuts to savings and home loan products.

Mozo’s personal finance expert, Rachel Wastell, says that while banks have been quick to slash savings rates, some mortgage holders won’t see relief for weeks.

“For many Aussies, their hard-earned savings are earning less interest before their mortgage relief even kicks in,” she says.

“The big question is: if banks can move so fast to cut savings rates, why does it take longer to pass on home loan reductions?

“The reality is, banks adjust rates in ways that best protect their bottom line – and right now, it’s savers feeling the pinch,” says Wastell.

With much of the focus on rate cuts and home loans, it’s easy to overlook other data drops. One such important economic indicator is wage growth, and how it might impact your money management.

Fresh ABS data shows wage growth slowed to just 0.7% in the December 2024 quarter – the lowest increase since March 2022. Cloud-based HR, payroll and benefits platform Employment Hero’s latest SmartMatch Employment Report found that median hourly wages grew by only 4.3% year-on-year in January 2025, down from a peak of 8.8% in August 2024.

State figures show the impact across Australia. Tasmania recorded the highest annual wage growth (3.9%), while New South Wales saw the lowest (2.9%). On a quarterly basis, WA, Victoria and South Australia experienced a rise (0.7%), in line with national average growth (0.7%).

Sluggish wage growth means incomes might not stretch as far, especially with the cost of living still biting. Strengthening your savings habits now – even small, consistent steps – could help you build a financial buffer.

See Mozo’s live tracker to learn which lenders are passing on rate cuts.

Following the recent decision to lower the official cash rate by 0.25% p.a., Summerland Bank says it will also be passing on rate cuts to variable home loan customers.

Summerland’s Premium Home Loan is actually a 2025 Mozo Experts Choice Award winner for being a ‘low cost home loan’.

Just take note, the interest rates on this loan will vary depending on the loan-to-value ratio selected.

For example, at the time of writing the Premium Home Loan on a <80% LVR (owner-occupied, $250k-$500k) is 6.29% p.a. (comparison rate 6.65% p.a.), as per the Mozo database.

So be sure to check this rate and those on other Summerland home loans as they will of course drop following this recent change.

See Mozo’s live tracker to learn which lenders are passing on rate cuts.

The stars continue to align, as Southern Cross Credit Union (SCCU) is reducing all standard variable home loan and business loan rates by 0.25% from 3 March 2025, following the RBA's latest move.

In the Mozo database we track SCCU bank home loans such as the Standard Variable Owner-Occupier Home Loan and the Standard Variable Investment Home Loan.

At the time of writing the interest rates on these loans are currently 7.48% p.a. (7.54% p.a. comparison rate) and 7.68% p.a. (7.54% p.a. comparison rate) respectively, but these will of course drop come 3 March.

And don't forget to check our Home Loans hub page where you can get up-to-date home loan rates from a wide variety of lenders.

Transport Mutual Credit Union (TMCU) will make a 0.25% reduction on all of its variable mortgage rates, effective from 21 February, 2025.

This means new rates will automatically apply to existing and new variable rate home loans.

The credit union says this rate reduction will provide welcome relief to its mortgage holders.

"By lowering our variable mortgage rates, we are ensuring that our home loan products remain competitive while helping our members with cost-of-living pressures," said TMCU chief executive, John Kavalieros.

See Mozo’s live tracker to learn which lenders are passing on rate cuts.

Online lender Sucasa has announced it will pass on the full 0.25% RBA rate cut to existing borrowers, with changes effective February 28, 2025.

This move aligns with several major lenders – including CBA, NAB, ANZ and Macquarie Bank – which will also lower rates on the same date.

As more lenders announce rate reductions, borrowers should keep an eye on the market for refinancing opportunities to secure a better deal.

See Mozo’s live tracker to learn which banks have passed on rate cuts.

ANZ Plus, the digital-only brand of ANZ bank has announced it will pass on the full rate cut of 0.25% to its Variable Home Loan customers.

This change will come into effect from 28 February 2025.

ANZ Plus will see rates on its refinance-only Variable Home Loan reduce from 6.09% p.a. (6.10% comparison rate*) to 5.84% p.a. (5.85% p.a. comparison rate).

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

Digital lender Unloan responded swiftly to the RBA’s decision by passing on the full rate cut to customers, effective today, February 21, 2025.

Unloan has adjusted rates a week or so ahead of most other providers.

For owner-occupiers with a loan-to-value ratio (LVR) under 80%, Unloan's variable home loan rate has decreased to 5.74% per annum (comparison rate 5.65% p.a.). Investors with an LVR under 80% will now benefit from a variable rate of 6.04% p.a. (comparison rate 5.95% p.a.).

In addition to rate reductions, the bank has once again come out triumphant in the Mozo Experts Choice Home Loan Awards, taking out an award for the third year running in the Low Cost Home Loan category.

See Mozo’s live tracker to learn which lenders are passing on rate cuts.

It’s not all home loan moves this week - new savings rates are also taking shape following the RBA decision.

This morning, NAB dropped rates on its Reward Saver and iSaver by 0.25%.

The base rate on the iSaver was 2.00% p.a., but this will drop to 1.75% p.a. effective from today.

Meanwhile, the special interest rate on the Reward Saver was 5.00% p.a. but this will drop to 4.75% p.a. across all deposit sizes.

Be sure to compare interest rates on our Savings Accounts hub page.

Bank of Queensland (BOQ) has announced widespread reductions across its savings account portfolio.

The bank is implementing a 25 basis point cut to its Future Saver, Fast Track Saver, Smart Saver, Bonus Interest, and Kids Savings accounts.

The WebSavings introductory rate will also decrease by 0.25 percentage points.

BOQ's Simple Saver account will also see a slightly larger reduction of 0.30 percentage points. These rates take effect as of today.

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

Good morning! Welcome back to our live coverage of interest rate moves following the RBA's rate cut decision on Tuesday.

To start with, People’s Choice credit union is passing on the full 0.25%p.a. rate cut to its variable rate home loans from 4 March 2025.

The company has specified that it will also apply rate changes to its 2-year fixed home loan rate by 0.20% p.a. and 3-year fixed rate by 0.10%p.a.

People’s Choice said it will confirm any changes to deposit products shortly.

Also, Heritage Bank is making the same cuts to the very same products under the Heritage label, as part of the same organisation. Heritage Bank merged with People’s Choice in 2023 to form a member-owned banking organisation.

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

Qudos Bank has announced it will pass on the RBA’s full cut of 0.25% across its variable rate owner-occupier home loans and investment home loans – effective from 27 February, 2025.

On top of that, Qudos also says it’s decreasing interest rates on its personal loans, variable car loans and credit cards by 0.25%.

Changes are coming to its savings accounts too. Qudos will axe 25 basis points off its Bonus Saver (bonus rate only), QSaver and Qantas Points Saver accounts.

That’s it for our interest rates live blog for Thursday, 20 February. Thanks for following along – we’ll be back tomorrow morning.

So, do you need to rely on RBA rate cuts in order to save money on your mortgage?

Not necessarily.

As part of our Home Loan Report, we examined variable interest rates across all lenders in our database to see how they stacked up against the winners of the Mozo Experts Choice Awards for home loans.

We found the average variable rate in the Mozo database to be 6.71% p.a. across all lenders, while the average variable rate among the Experts Choice Award home loan winners is 6.01% p.a.

That’s a drop of 0.70%, which is close to almost three RBA cuts of 0.25% each.

In real terms, this could translate to about $217 saved in monthly repayments on a $500,000 loan if you were to switch from the average variable rate to a Mozo-winning rate.

If you think you could be getting a better deal, it might be time to compare home loans and see how much you could save.

| Lender type | Average rate (p.a.) | Monthly repayment |

|---|---|---|

| All lenders in the Mozo database | 6.71% | $3,441 |

| Big Four banks (ANZ, CommBank, NAB, Westpac) | 7.15% | $3,582 |

| Mozo Experts Choice Award Winners | 6.01% | $3,224 |

Source: Mozo database. Accurate as at 12 Feb 2025, average variable rates for owner occupier, principal & interest home loans, interest paid over a 25 year loan term, 80% LVR, $500,000 loan amount. Average for MECA winners based on the rates of MECA winning products on 12 Feb 2025, using the same criteria.

Read more: RBA cuts rates for the first time in four years – is now the time to refinance?

A cash rate cut of 0.25% may only shake out to be a small saving for some Australian borrowers, but Mozo’s research suggests the RBA’s cut could also drive an uptick in those looking to refinance their home loan.

According to our survey data, almost half (49%) of mortgage holders are weighing up their options following the RBA’s decision to cut.

At the same time, 48% of borrowers surveyed said they aren’t planning to refinance after a cut to the cash rate.

Even if you don’t have plans to refinance your home loan, it’s worth looking at our rate change tracker – you can use it to see which of the banks are passing on the rate cut.

| Response | % of mortgage holders |

|---|---|

| No | 48% |

| Considering it | 35% |

| Yes | 14% |

| I have recently refinanced | 4% |

| Source: Mozo commissioned a nationally representative survey of 1,021 Australian mortgage holders aged 18 years and over, with information collected between December 2024 and January 2025. | |

In the flurry of discussion that follows any RBA rate decision, the bigger picture can easily be lost.

Who, after all, benefits from this 0.25% rate cut?

Perhaps the biggest beneficiaries are those with a variable home loan, who for the past couple of years have endured higher interest rates than they might have expected following the pandemic-era low of 0.1%.

After 13 straight rate hikes by the RBA over 2022 and '23, many with a larger mortgage have found their budget pushed to the limit. So where home loan providers have passed on this latest rate cut of 0.25%, affected homeowners are no doubt rejoicing.

Meanwhile, some first-time buyers looking to jump into buying a property might also see a chance to scoop up a cheaper home loan rate ahead of their first purchase. They too should be pleased.

But there will be a portion of people who get left on the sidelines in all of this, because as the property market picks up, as is typically the case following a rate cut, property prices also tend to rise.

If this happens quickly in some locations, as we’ve seen in past years, price gains can outpace the benefit of a single rate cut.

Mozo’s banking expert Peter Marshall agrees that we can expect house prices to climb - and while wage growth continues to be subdued.

"Yes, cutting rates only helps a portion of the population - those without a mortgage and particularly savers are mostly worse off,” he said.

It's for this reason we always suggest that comparison is the best tool in your personal finance toolkit. You don't need to stand pat with the product you have. Compare home loans and savings accounts on our respective hub pages.

With the RBA lowering the cash rate by 0.25% p.a., both BCU Bank and P&N Bank are passing the full cut to all variable home loan customers from 5 March, while also reducing rates on a wide swath of their savings accounts.

Given that both banks are part of the same customer-owned banking group, Police & Nurses Limited (PNL), it makes sense they’re taking a similar approach this time around.

Not every savings rate is changing, so check with your bank to see if your account is affected.

IMB Bank will lower its variable home and business loan interest rates by 0.25% following the decision by the RBA to cut the cash rate.

These reductions are effective from March 4 for new and existing borrowers.

IMB Bank chief executive officer, Robert Ryan, said, “We understand that cash rate increases in recent years have put pressure on our borrowers and this rate reduction will provide welcome relief for the many members and small businesses around Australia who bank with IMB.

“Although our members have managed previous cash rate increases well, we are pleased to be able to pass on the RBA rate reduction in full and maintain some of the most competitive interest rates in Australia.”

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

Great Southern Bank will cut variable home loan rates by 0.25% p.a. for most of its owner-occupied and investor home loans.

You can check how their home loans stack up against the competition on our Home Loans hub page.

Mozo’s live tracker follows which lenders have passed on rate cuts.

Another home loan move ... Beyond Bank will decrease home loan interest rates by:

Rates for these products will change on 4 March 2025.

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

MyState Bank has cut variable home loan rates for new and existing customers across owner occupied and residential investment loans as well as commercial loans by 0.25% p.a., effective from 4 March 2025.

The rate cut also extends to residentially secured line of credit products for existing borrowers.

For deposit customers, the bank will be reviewing interest rates and will advise of any changes, as per its website.

Check out Mozo’s live tracker to see which lenders passed on rate cuts.

AMP Bank is making changes to its variable home loan rates for new and existing owner occupiers and investors, following the RBA cut to the cash rate on Tuesday.

These changes will be effective 28 February for new customers and 3 March for existing customers.

"We recognise that previous RBA cash rate increases have been challenging for household budgets and that customers are looking forward to interest rate relief," AMP said on its site.

"Changes to the official cash rate is one of several factors that impacts our pricing decisions. Other factors include the direct implication of the cash rate movement to the cost of borrowing, market conditions, as well as a desire to balance the interests of homeowners and savers."

Don’t forget to check out Mozo’s live tracker to see which lenders passed on the cut to borrowers – and which haven’t.

This just in… AMP Bank is reducing variable interest rates across a range of its deposit products following the RBA's 0.25% cash rate cut, effective tomorrow, Friday 21 February 2025.

Here’s what has changed:

Term deposits do not appear to be affected by this cut.

Don’t forget to check out Mozo’s live tracker to see which lenders passed on the cut to borrowers – and which haven’t.

Bank of Sydney will reduce standard variable loan interest rates for new and existing customers by 0.25%, effective 12 March 2025.

Affected customers will receive direct written communication outlining changes to their interest rate and minimum repayment amount.

Don’t forget to reach out to your provider to learn more about rate changes and how they might affect your loan and repayments. Additionally, now is a great time to compare home loan rates. With banks lowering their rates, you may find a better deal elsewhere.

Discover more about the decision and check out Mozo’s live tracker to see which lenders passed on the cut to borrowers – and which haven’t.

Just in, Auswide Bank is cutting its term deposit rates by 0.25% p.a. across all terms, the bank says.

With these changes, the highest Auswide rate is 4.70% p.a. For 5 months, as per the Mozo database.

So far, we’ve seen a lot of savings account cuts, but not much action on term deposits. Though we knew term deposits were potentially on the chopping block.

If you’re planning to get ahead of rate cuts by locking your cash away, now might be the time to do it while rates are still fairly good.

Bank First will be decreasing the interest rates on both savings and home loan products, the bank has just announced.

Rate changes are as follows:

Savings - effective 27 February, the interest rates on a range of savings products will decrease by up to 0.25% p.a. followed by a decrease to the bonus interest rate on the Bonus Saver account and First Home Bonus Saver by 0.25% p.a. on 1 March.

Variable Home Loans - effective 27 February, home loan variable interest rates will decrease by 0.25% p.a.

New interest rates will be displayed on 27 February through Internet Banking and the Bank First App.

See Mozo’s rate change tracker for more updates.

Just in at our news desk, BOQ will reduce variable home interest rates by 0.25% per annum (p.a.) from 7 March 2025.

Meanwhile, GMCU will also pass on the rate cut in full from 1 March.

Check out Mozo’s live tracker to see which lenders have passed on the cut to borrowers.

Good morning and welcome back to our live blog! It's been a busy week of rate cuts to home loans so far and we expect more of the same today.

Let's start with ME Bank. Following Tuesday's RBA decision, ME will reduce its variable home loan interest rates by 0.25% per annum (p.a.) from 8 March 2025, the bank says.

Founded in 1994, ME was formerly Member’s Equity Bank and is now owned by Bank of Queensland. It has a range of home loans and was previously a Mozo Expert's Choice Award winner.

Learn more about the RBA decision and check out Mozo’s live tracker to see which lenders have passed on the cut to borrowers – and which haven’t.

It certainly was a busy day in home loans and savings, here are some of the main headlines:

That's a wrap! Thanks for joining us today, see you back here tomorrow for more interest rates coverage.

Non-bank lender Resi has also confirmed that the recent RBA rate cut of 0.25% is being passed on in full to all new and existing Essentials Options customers.

Existing borrower rates will decrease effective 28 February 2025. All other Resi white label loans are currently under review, according to the mortgage provider's website.

Also of note today, Homestar Finance says variable rates for its existing home loan customers will reduce by 0.25% p.a., effective 28 February.

Be sure to compare home loans on our hub page.

Brisbane-based lender Firstmac says its variable home and car loan interest rates will decrease by 0.25% effective from the 4 March 2025.

This applies to new and existing customers.

Firstmac also owns Loans.com.au, which happens to have won a 2025 Mozo Experts Choice Award in the 'first homebuyer' category for its Variable Home Loan 90 (P&I), LVR <90%. At the time of writing, that loan has a 6.04% p.a. variable interest rate (6.08% p.a. Comparison rate). Its rate will also decrease by 0.25% p.a. on 4 March 2025.

Discover more about the decision and check out Mozo’s live tracker to see which lenders passed on the cut to borrowers – and which haven’t.

With several banks announcing rate cuts, it’s important for borrowers to take a beat and reach out to their banks. While many banks will notify variable home loan customers directly by email or letter about their new minimum repayment details, it’s still sensible to check in with your lender to clarify how these changes affect your loan and repayments.

Clarify your new repayment details: Depending on the size of the rate cut, your repayments may decrease, but it’s good to ensure your new repayment schedule is correct and reflects the change.

Example: If your home loan is $400,000 and the rate cut is 0.25% p.a., your new minimum repayments might be lower, but you want to be sure you're not overpaying or underpaying based on the adjusted rate.

Confirm the impact on your loan balance: Rate cuts can also affect the total interest you’ll pay over the life of your loan. While the immediate effect might be a decrease in your monthly repayments, it’s wise to confirm how these changes affect your overall loan balance.

Example: A reduction in interest could result in a lower total loan cost over the life of the loan. If you’ve been considering paying off your loan faster or making extra repayments, now might be the time to check in with your bank.

Ask any questions you may have: If you're uncertain about how rate changes may affect your loan or whether you’re getting the best deal, don’t hesitate to ask for details. The clearer you are about your loan’s terms, the better you can manage your finances moving forward.

Example: If you're running a small business with a variable rate loan, the rate cut could affect both your cash flow and your repayment strategy. Ask your bank if there are any other options that could help you save more, such as switching to a fixed rate or a different loan product.

When a bank lowers variable home loan rates for existing customers, the change typically happens automatically on the effective date – usually around 10 to 14 days after the announcement. Interest is calculated daily, so as soon as the rate drops, you'll start paying less interest.

Now is a great time to compare home loan and business loan rates among different providers. With banks lowering their rates, you may find a better deal elsewhere. This is especially true if you’ve been with the same lender for a while and haven’t explored your options recently.

You may be able to negotiate a more competitive rate with your current bank, or switch to a lender that offers more favourable terms.

Discover more about the decision and check out Mozo’s live tracker to see which lenders passed on the cut to borrowers – and which haven’t.

CommBank will decrease interest rates on two of its savings accounts products effective 28 February 2025, the big four bank says.

The new rates are as follows:

You can check how these rates stack up against the rest on our Savings Accounts hub page.

.jpg)

Borrowers are getting much needed relief from the cash rate cut with a raft of lenders announcing downward revisions on interest.

On 1 March 2025, Australian Mutual Bank is planning on decreasing variable home loan rates by 0.25% for new and existing borrowers.

Auswide bank will cut rates on existing home loans by 25 basis points on 28 February 2025 while on 27 February, Bank First will cut variable home loans by 0.25%.

Meanwhile, Greater Bank will cut variable home loans on 7 March 2025 by 25 basis points. Finally, Teachers Mutual Bank will see 0.25% cuts to variable home loans for new and existing borrowers on 28 February.

See Mozo’s live tracker to learn which lenders have cut interest rates.

HSBC will decrease its variable home loan interest rates by 0.25% p.a., effective from Monday 10 March 2025, the bank reports.

Currently in the Mozo database HSBC's Discounted Home Value Loan for owner-occupiers (P&I) with an LVR of 70-80%) is at 6.09% p.a., for example.

Meanwhile, the HSBC site advertises 6.14% p.a. on its owner-occupier (P&I) home loan (with an LVR of 60% or less).

Be sure to read our review of the Discounted Home Value Loan.

See Mozo’s rate change tracker for more updates.

Through this morning a number of banks and financial institutions have announced that they’ll be trimming their variable home loan interest rates on the back of the RBA’s decision to cut the cash rate to 4.10%.

From 4 March 2025, Westpac will reduce the variable rate on cash rate linked business loans and overdrafts. If you're a customer and have any questions, you can contact the bank to request a call back.

Defence Bank will cut both new and existing variable rate home loans by 0.25% p.a. This change will be effective Thursday 27 February 2025.

Online Australian lender homeloans.com.au confirmed that it would be passing on the full rate decrease – a reduction of 0.25% p.a. – to all existing and new customers on all variable rates, effective 5 March 2025.

Plus, Transport Mutual Credit Union (TMCU) announced a 0.25% reduction in all variable mortgage rates, effective 21 February 2025.

See Mozo’s live tracker to learn which lenders have cut interest rates.

Newcastle Permanent and The Mutual Bank have both announced they will be passing on the RBA’s full rate cut of 0.25% to borrowers.

Newcastle Permanent says its new home loan variable interest rates will be effective from 7 March, 2025.

The bank says its current variable home loan customers will be notified of their new minimum repayment amount by email or letter.

Those with a variable home loan through The Mutual Bank will get their rate relief a little sooner, with a 0.25% p.a. decrease coming from 4 March, 2025.

The Mutual Bank has also noted that its savings deposit rates are currently under review.

See Mozo’s rate change tracker for more updates.

Westpac says it will reduce its Westpac Life savings account rate by 0.15%, down to 4.75% p.a.

New customers to Westpac eSaver will also see a 0.25% p.a. cut the 5-month introductory rate to 4.75% p.a.

Both account rate changes will be effective 28 February.

So far, the other three of the Big Four banks haven’t released a statement regarding savings accounts, but we expect to see further reductions in the coming days.

You can compare some of the highest rate savings accounts and term deposits we track on our database by heading to the hub pages.

(1) (1) (1) (1).jpg)

This morning Ubank announced it will be reducing its Neat and Flex variable home loan rates by 0.25% p.a. effective from 27 February 2025.

Ubank is owned by NAB and is a digital-only bank, with home loan applications done entirely online.

There are a number of Ubank home loans on the market so best to check how each stacks up with these cuts, but as an example, its Flex and Neat home loans for owner-occupiers (P&I) LVR 70-80% offers 6.14% p.a. at the time of writing, as per the Mozo database.

See our full coverage and check Mozo’s rate change tracker for updates.

Good morning and welcome to Mozo’s live blog. I’m senior writer Peter Terlato. Today we’ll be following up on the Reserve Bank of Australia’s (RBA) decision to cut Australia’s official cash rate – from 4.35% to 4.10%.

We’ll be covering any announced changes to home loan rates, savings and term deposit rates, as well as providing a breakdown of what these changes mean for borrowers, savers, and investors. Stay tuned for helpful insights and analysis.

Let’s dive in!

The Reserve Bank has offered mortgage holders some relief with its first rate cut in four years but signaled that a tight labour market and the risk of disinflation stalling could stand in the way of further reductions.

At the press conference following the decision yesterday, RBA Governor Michele Bullock was quick to push back against market expectations of multiple cuts ahead. Australia’s major banks wasted no time, passing the full rate cut onto home loan customers.

“I want to be very clear that today’s decision does not imply that further rate cuts along the lines suggested by the market are coming.”

“We have to be careful not to get ahead of ourselves. Some inflation pressures remain, and cost-of-living challenges are still front of mind for many.”

– RBA Governor Michele Bullock

In its monetary policy statement, the RBA highlighted “unexpectedly strong” labour market data, which “tightened a little further in late 2024”. Additionally, “productivity growth has not picked up”, implying that the cost of paying workers is rising faster than the amount of work they’re producing – key factors that could delay any immediate future easing.

Discover more about the decision and check out Mozo’s live tracker to see which lenders passed on the cut to borrowers – and which haven’t.

One of Australia’s largest and most influential financial institutions, Macquarie Bank, joins the growing list of financial institutions announcing cuts to home loans.

Macquarie Bank said it will be decreasing its variable home loan reference rates by 0.25% p.a., effective from 28 February, 2025.

Ben Perham, Head of Personal Banking at Macquarie Bank, said: “The number of customers choosing to bank with Macquarie has continued to grow strongly through recent interest rate cycles. With mortgage brokers voting us the best lender for the past five years and savers responding positively to our no 'hoops or catches' everyday banking savings accounts, we’re confident our offering will continue to resonate strongly with customers across Australia.”

See our full coverage and check Mozo’s rate change tracker for updates.

That's a wrap for our interest rates coverage for Tuesday, 18 February. We’ll see you in the morning for more rate cut announcements and market insights. Stay safe on your commute!

ING, Australia's fifth largest financial institution, has announced a decrease of 0.25% p.a. for all existing customers with a variable interest rate home loan, effective 4 March, 2025.

Additionally, Suncorp Bank will decrease variable interest rates by 0.25% p.a. for home loan customers, effective 28 February 2025.

See our full coverage and check Mozo’s rate change tracker for updates.

With the RBA cutting the cash rate by 0.25%, it's time to review your own home loan.

The best place to start is to see the difference between your current rate and one that's notably lower.

Here's a quick look using the Mozo home loan comparison calculator on a typical owner-occupier loan (P&I) over 25 years:

First loan

Loan amount: $400,000

Interest rate: 6.25% p.a.

Monthly repayments: $2,969

Total interest and fees paid: $440,554

Second loan

Loan amount: $399,294

Interest rate: 5.75% p.a.

Monthly repayments: $2,831

Total interest and fees paid: $399,294

The difference is significant: you would save $41,260 over the 25 year term.

This is just one example of the type of rate difference you could come across while comparing. Head over to our Home Loans hub to find some of the leading interest rates in the Mozo database to do some calculations of your own.

Westpac was the first of the Big Four to announce a cut to its mortgage rates. The bank revealed that it would pass on the rate cut in full (-0.25% p.a.) to variable rate home loan customers from 4 March, 2025.

The Commonwealth Bank of Australia (CBA) has also adjusted its mortgage rates. Australia’s largest bank will decrease variable home loan interest rates by 0.25% p.a., effective 28 February 2025.

NAB will reduce its standard variable home loan interest rate by 0.25% p.a., effective 28 February, 2025.

ANZ will cut variable interest rates across Australian home loans by 0.25% p.a., effective 28 February, 2025.

Here’s a list of other banks and providers who’ve announced cuts:

See our full coverage and check Mozo’s rate change tracker for updates.

The Reserve Bank of Australia (RBA) announced its first rate cut of 2025, reducing the cash rate to 4.10% at its February meeting.

This move comes on the back of easing inflation, prompting the central bank to shift its approach and offer some relief to borrowers.

This decision marks the first cut in the cash rate since November 2020. Between May 2022 and November 2023, the RBA embarked on a series of aggressive rate hikes in response to soaring post-pandemic inflation.

See our full coverage and check Mozo’s rate change tracker for updates.

If the RBA decides to cut the cash rate by 25 basis points at today’s meeting, mortgage holders and prospective buyers will be expecting a reduction in home loan interest rates. However, there’s no guarantee that banks will pass on the full cut to borrowers.